What makes people run into investments

with everybody else doing the same,

when common sense dictates otherwise?

In this chapter, we’re going to understand why Mental Accounting and Herd Instinct are so misunderstood and often misplaced in the business of trading and investing.

Let’s recap the four key points of Behavioural Finance from the previous chapter:

- Mental Accounting is about position and sizing with regard to the reason for investing relative to risk.

- Herd Instinct is the decision making process from the influences of the masses which have no bearing on risk or reason.

- Benchmarking allows the investor to make comparisons to get a quantitative reason for their choice of investment.

- Lastly, Pride/Ego is about the need to be right with no regard to profit and/or loss or accuracy in comparison to peer performances.

What we’re NOT going to do is discuss how these conditions can help you to make money. Rather, we’re going to investigate the pitfalls of each of these conditions and add in a few more conditions to see how we can understand them better so that we don’t lose money.

QUESTION: Is it possible to make half your money yield more in Investment B than the rate of interest being levied on the other half in Investment A?

In the most common example of Mental Accounting that I can think of, nine in ten people would prefer to hold a mortgage than settle in full for the property they own when they can obviously afford it. It is obvious that the debt will add up to significantly increase the overall spending on the property but when it comes time to sell, nine of the nine won’t consider the interest they’ve paid when settling on a sale price. The price they settle for is always based on the most recent price that was closed on a neighbouring property. This is Benchmarking that is never considered during Mental Accounting for which the logic behind the accounts never adds up in the end.

In this scenario, the investor holds a mortgage in spite of the financial advantage of being able to pay in full. The intention is to invest the money he holds for his instalment plan, into high-yielding investments while stretching out the mortgage. The objective is to count on the yield of the invested money to outpace the rate of interest on their property over the period of the mortgage.

Whether it works out in the end or not, the investment’s yield is never considered as part of the final plan and neither is the mortgage’s interest. For all that was made or lost, the final price for selling is always against some benchmark (set by the neighbour) that was never considered during the Mental Accounting phase.

The proof is in the pudding, as they say. All you have to do is listen in or recount previous conversations about such topics. They always go along the lines of, “I bought the house for $XXX,XXX.00 and sold it three years later at $X,XXX,XXX.00 for a X0% profit.”

Furthermore, when the investment loses money, no one will consider if the yield was sufficient to cover the interest. In fact, the last thing, if at all, on anyone’s mind in a losing situation is Mental Accounting.

The situation arises from the fact that when we start out investing, we are Mental Accountants. But when it is time to sell, either for a profit or loss, we become emotional. The two sides of the brain don’t work as one.

Another way to look at this is when we invest, we’re thinking with our head but the decision to sell comes from the heart.

Another common example is when such investors fund their U.S. account with a foreign currency and refuse to “lose out” on the exchange rate’s spread. They will find ways to “hedge” their funding to “contra” the slippage without considering that opening the hedge also carries a slippage and commission/execution costs, never mind that they just increased their risk with another position.

Mental Accounting does have its rightful place in Trading, Investing and Business. However, when emotions take over in the middle of the battle, Mental Accounting is a misplaced event and an always forgotten principle.

QUESTION: What makes the masses believe that putting money into some investment plan sold at investment shows, expos and fairs are actually good investment opportunities? Is it the massive returns they promise? Is it the perceived “safeness” of the investment? Or is it because “everyone else” is getting into it?

Remember this?

FACT: If the investment was that good, you wouldn’t have a chance to buy it at Expos and Fairs simply because it would have sold out long before the mass public had a chance. You probably wouldn’t have heard about it either because the Insiders snapped it up before you even knew about it. If they’re selling it at Expos and Fairs, it is because the insiders, banks and institutions did not buy it and the big time investors weren’t interested nor impressed by it.

Time and again, I meet students who come to me because of a very common fatal flaw; They simply followed what everybody else was doing and what the media said was a good buy.

This is also a common practice when we consider some banking fund or unit trust. We tend to feel more “comfortable” when we hear that everybody else is buying this product. This is Herd Instinct. It somehow gives us a sense of security knowing that everyone has faith in the product … but we don’t know that for a fact and basically take the bankers word for it.

The strange thing about Herd Instinct is that people feel better knowing that they are not the only victims when something goes wrong. But the unacceptable fact remains that you lost money along with everyone else.

YOU LOST!

Does accepting that fact make you feel better now? I’ve heard conversations amongst such people where one person said “Lucky I didn’t lose a lot. The other guy lost more than me.” How is that supposed to make you feel better when your account has undoubtedly lost money regardless of how much someone else lost? Is that a Pride or Ego issue or is it Benchmarking I am hearing because that certainly isn’t Mental Accounting.

Does accepting that fact make you feel better now? I’ve heard conversations amongst such people where one person said “Lucky I didn’t lose a lot. The other guy lost more than me.” How is that supposed to make you feel better when your account has undoubtedly lost money regardless of how much someone else lost? Is that a Pride or Ego issue or is it Benchmarking I am hearing because that certainly isn’t Mental Accounting.

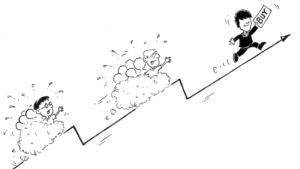

Either way the price for Herd Instinct is always a mass migration of money. The lure of “strength in numbers” is much too convincing to ignore when taking risks. However when you think objectively about it, it is obvious that you’re much too late if “everybody had bought it” by the time you consider buying it.

Then you have FOMO, the fear of “missing out” … yet another factor that plays on the minds of the herd. Once again, neither Mental Accounting nor Benchmarking is considered when following the herd blindly. This is obvious because the price has already made handsome gains for those who got in earlier. You’re too late. But all that matters is that you get on that irrational bandwagon and not get left behind.

Then you have FOMO, the fear of “missing out” … yet another factor that plays on the minds of the herd. Once again, neither Mental Accounting nor Benchmarking is considered when following the herd blindly. This is obvious because the price has already made handsome gains for those who got in earlier. You’re too late. But all that matters is that you get on that irrational bandwagon and not get left behind.

At this point, ask yourself if it really matters that you missed this ride. You’re obviously too late to jump on so why not wait for the next opportunity when prices are more reasonable? Why buy the high when it is always stated that we should buy low and sell high?

It is only in hindsight that we see the insanity of our actions. So why bother to commit to such idiocy in the first place?

You have obviously heard these stories many many times over. Yet we keep hearing new versions of the same story every so often. It’s like people never learn … or do they? The truth is that new “suckers” mostly get their baptism of fire by making the same old mistakes for the first time. I doubt very much that someone who has been bitten badly before would opt to make the same mistake twice.

But then, you do get the odd exception to the rule …

QUESTION: Why do some people keep going back to the same toxic plan that got them screwed previously?

Lehman Mini Bonds, Pinnacle Notes, Swiber, Hyflux … you’ve read the stories and you’ve heard the nightmares. Though the product names changed, the same naive players did not.

The temptation of making the big money always attracts the same breed of gamblers mostly because of what I term as “The Revenge Trade”. This is a case of someone losing money and wanting to make it all back with the “next big thing”. Their greed blinds them from logic. They often jump into the next big headline quicker than they jumped into their first loss. This is because they learnt that getting in too late will be costly.

This is misplaced Mental Accounting again. If the investment wipes out, whether you got in early or late, you’ve lost your whole investment anyway.

What this investor should have done after the first loss was to investigate the mistakes and oversights that made that investment wipe out. Then use that experience to make better judgements the next time instead of looking to make the quick revenge.

The simple task is to analyse the worst case scenario of any investment before taking the leap. If the worst case can be calculated to a minimum, then it might be worth considering. But if the worst case is a total wipe out, then why bother? Look for something safer – and safer also means “under the radar” which means it won’t be headline news.

Here’s an example;

If you have to decide between two funds …

-

- Several unknown new tech companies (touted to be the next Amazon, Facebook and Google) with a potential to return 14% per quarter

- A hedged fund of indices like the S&P 500, Nikkei 225 and ASX 200 with a historical average return of 6% per quarter

… which would you choose?

By assessing worst case scenarios, the main threat would be whether the fund can wipe out. Indices don’t wipe out. Stocks do.

By analysing risk based on historical performance, the new tech companies don’t have enough history to give you any sort of comfort level whereas the indices have decades of data that tend to repeat themselves.

By considering macroeconomic factors for leadership indications, the new tech companies don’t have enough earnings record to prove their worth nor the time-tested fundamentals to support their price. Indices … I think you get the picture.

A lot of times, the victims of such wipe outs are lulled into complacency by the fact that the security is regulated and endorsed by some established institution or central bank or exchange commission and is highly rated by a well known rating agency. It’s like thinking that a particular car is a good buy because it passed the government safety requirements, Lewis Hamilton rated it highly and you’re not likely to die in an accident.

For your information, all this is a given – all traded securities have to be regulated by an exchange commission, treasury bonds are underwritten by central banks and the issuers and/or underwriters of a security is always some bank or financial institution. Don’t allow such “credentials” to influence you into thinking it is a good/safe investment because these are basic compliance procedures. Because in spite of all the regulation, endorsements and ratings, it can still fail.

And that car Hamilton vouched for? You can still die in it given the worst circumstance.

Let’s not forget that;

- Moody’s put Lehman Brothers’ investment-grade A2 rating “on review” a mere five days before it filed for bankruptcy.

- Standard & Poor’s gave American International Group (AIG) an investment-grade A rating less than a week before the insurance company was nationalised.

- Merrill Lynch and Bear Stearns sported investment-grade ratings when they were rescued by Bank of America (BAC) and JPMorgan Chase (JPM), respectively.

- Fannie Mae and Freddie Mac had highly coveted AAA ratings at the time they were forced into conservatorship.

Use logic and common sense and if you have any doubt, simply don’t commit. If you don’t know enough about what you’re buying, research it thoroughly or don’t buy it at all. Never allow your greed and impatience compromise your hard-earned life’s savings. And never ever be tempted by what the masses are doing because that’s a sure sign that you’re too late.

Would you risk your life on an old suspicious looking bridge after everybody else has crossed it and ruined it, even if your government told you it was still safe?

However, if there is no endorsement or regulation, that’s an obvious sign to walk away.

Such was the case with Malaysia’s MoneyGame a few years ago. What made it more of a spectacle was that it was an obvious Ponzi scam and yet the masses still flocked into it knowing the kind of risks they were taking. The MoneyGame played heavily on the minds of the masses by using Herd Instinct as their influential marketing tool.

The media, market manipulators, sales and marketing experts know how to get your commitment by exploiting your misplaced Mental Accounting and Herd Instinct to make you irrational and rash. They will show you a few success stories about their winners. They will tell you what you want to hear and show you what you want to see. They will use credentials and statistical track records to impress and convince you. They will repeat it often and repeat it loud because the more often you hear and see it, you’ll eventually be convinced.

But you still have to do your job. Do the hard work and get your research done. No one is going to care more about your money than you so why trust anyone with their opinion? Be smarter about your money because no one else will.

Next week, we finish this three-part series with Behavioural Finance For Beginners – Part 3.

Have a great weekend!!

Copyright© 2021 FinancialScents Pte Ltd

• • • • •

Join our next Pattern Trader™ Online Tutorial in March 2021.

INQUIRE NOW!

After 15 years of educating, mentoring and supporting hundreds of participants (annually) in the arts and sciences of Finance and Economics, the Pattern Trader™ Tutorial has evolved to become the most exclusive and sought-after boutique-styled class that caters to retail individuals, institutional professionals, businesses and families that are serious about their finances and their prospects as we move into the future.

The small class environment and tutorial-styled approach gives the Tutorial a conducive environment that allows for close communication and interaction between the mentor and the participants.

The hands-on style makes the Tutorial very practical for anyone who requires a start from the ground up. It is the perfect beginning for anyone who wishes to take that first step in improving their financial and economic literacy.

This is what past graduates have to say …

“I was introduced to PTT 10 years ago but put off the pursuit to take up this program due to family & work commitments. It’s better late than never and I have never regretted one bit having attended the Tutorial with Batch 96. In retrospect, I realised that it was a waste not doing this sooner and missing out all the good windows of opportunities over the last decade.

The course fee may appear to be a premium but in my personal view, this program is almost as good as taking up a MBA program to prepare you for the real financial world. It arms you with a good understanding of Macro Economics, as to how the world really moves money. The program has great content, is well structured and delivered in a systematic way where the whole puzzle around trading and investing adds up by the end of the program after 2 intensive weekends.

The no holds barred, no BS delivery provides a rude reality check about what real trading is all about. The excellent support, guidance and mentorship offered readily by Conrad is what makes the program unique and different from many other programs in the market. No hard-selling tactics and no hidden agendas in the program that will turn you off.

There are very methodical steps, techniques and guidelines on how to make CONSISTENT wins. The focus is on consistency of results and not a “get-rich-fast-and-furious” approach. Definitely not for the impatient and disillusioned ones who are looking for the holy grail to “sure-win-trading” because there are none to be found here. This is one program that would fit well for all levels of traders whether you are experienced, a newbie or even an institutional trader.

A great program I would recommend for anyone who is serious about trading consistently.”

~ C.E. Chng

~~~~~~~~~~~~~~~~~~~~~~~~~~~

“I will highly recommend this course and its Specialist Programs to anyone who wants venture into online trading. Conrad is so knowledgeable and no other courses have such massive contents, such as the Macros, Money-flow, Seasonality, Risk management, Fundamental and Technical Analysis, entry setup, etc etc.

This is really a Holistic Financial Education which applies to our daily-life both online and offline. I want to highlight the support provided by Conrad himself personally. “

“He will personally answer any and all queries or problems that we students faced. Personally, I have attended some other courses taught by other gurus, but really, there are none like Conrad.”

~ Desmond Lee

If you’re looking to make a huge difference in your financial life and get the most value for your education investment, there’s no better choice than the time-tested and well reputed Pattern Trader™ Tutorial.

Join our next Pattern Trader™ Online Tutorial in March 2021.

INQUIRE NOW!

Download our promo slides here:

The Pattern Trader™ Tutorial 2021

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Write to conrad@finscents.com for queries and further information