The original article was featured in the Straits Times on Sunday 16 August 2020 (Click to subscribe).

I have written many similar pieces with regard to financial management over the years but it seems people indeed never change as with each new generation of working class adults that emerge, the same filthy habits prevail regardless of the lessons taken from the many previous generations before.

Once again, we’re in a bubble that’s about to explode in spectacular fashion and once again, we find the same kind of people on the verge of financial dire straits, not a dozen years after the last big financial meltdown. They’re not the same people but the same KIND of people. And I used to be one of them until I learned my lesson the hardest way possible. You’ll find my story very familiar.

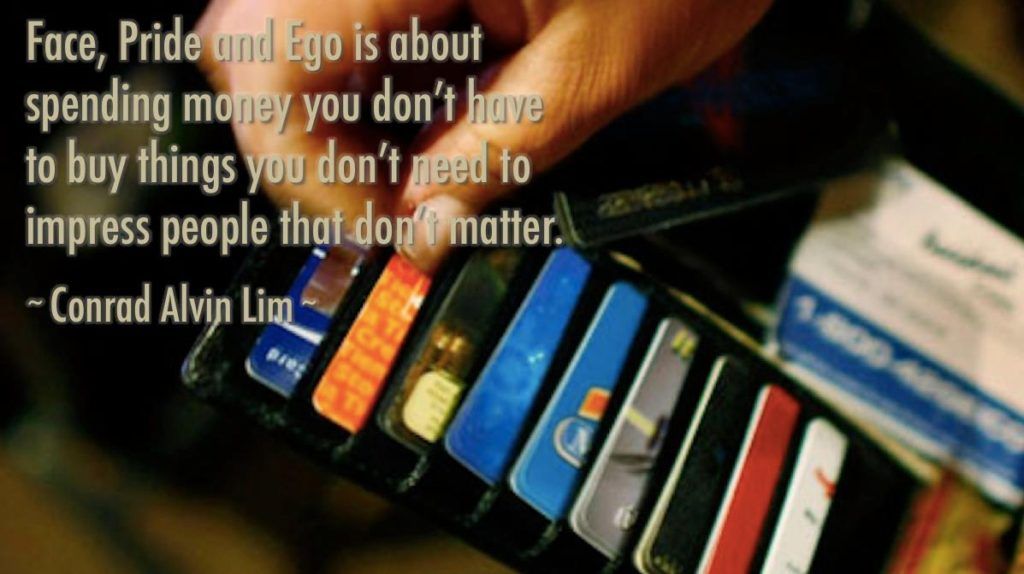

It is heartbreaking because it really is needless and could have easily been avoided if not for three things that always send these people down the path of financial doom; Face, Pride & Ego.

It is my wish that people learn to be happy with what they have instead of yearning for things that they don’t need to impress people who don’t matter. Spend, by all means, if you have the means to spend. But if you don’t, no one is going to disrespect you for being prudent and frugal.

Remember; Money in the bank is a growing, liquid asset whereas debt in the wallet can be a growing liability for life.

Overspending is the main reason that many people are in debt

Original article from the Straits Times on Sunday 16 August 2020 (Click to subscribe).

They are rich, successful and highly educated. These three men share so much in common that they could end up as buddies if they ever met.

All three are in their 40s, have tertiary degrees, are married and hold top jobs in their respective organisations that coincidentally pay them about $30,000 each a month.

With such high incomes, it is fair to assume that all three are likely to share the same lifestyle of living in million-dollar private homes and driving expensive cars.

Things should have been working well for them financially until they made the mistake of over-leveraging their means. As a result, they now also share the fate of being in financial ruin.

One gambled his wealth away and ended up with $1.7 million in debt, another made an investment loss to the tune of $2.5 million, while the last ended up with $2.3 million in business and investment debt.

The first man was put on a debt management programme and paid back what he owed after seven years. The other two men have yet to finish paying off their dues.

These three cases in the ledger of debtors of Credit Counselling Singapore (CCS), a charity dedicated to helping people avoid financial disaster, present an important lesson: If you spend without any regard for what you have, you will be in serious trouble even with a high income.

MANY FAMILIES HAVE POOR FINANCIAL PLANNING

The downturn has revealed that tens of thousands of families here do not have sufficient savings, let alone retirement planning, to cushion them when things turn for the worse.

They use loans to support a lifestyle that they may not be able to afford, and when the pandemic hit, they did not have the means to keep up with the repayments.

The number of people who have asked to defer loan repayments paints a grim picture of widespread financial trouble. Data from the Monetary Authority of Singapore shows:

- 34,000 home owners have asked to stop paying their loans and interest until December;

- 2,100 people have problems paying renovation and education loans;

- More than 6,200 have asked to convert high credit card debt into term loans on lower interest rates;

- Around 3,200 vehicle owners want help with loans;

- About 25,000 policy holders have asked to defer premiums for life and health insurance for six months; and

- About 600 people have asked for instalment plans to pay general insurance policies that are normally paid in lump sums.

But deferment is only a temporary relief; the loans and premiums will eventually have to be paid and the postponement actually incurs interest costs that mean bigger outstanding balances.

HOW PEOPLE FALL INTO DEBT TRAP

CCS has helped more than 32,000 people since 2004 to manage their finances better.

Of this group, around 22,000 have been put on management programmes that help them slowly pay off their debts.

To date, only about 6,000 have completed the programme. This means more than 16,000 people are still trying to pay off sizeable debts chalked up before the pandemic.

Most of these debtors are in their 30s and 40s, and about 70 per cent of them are men.

In total, people under the CCS programme owe almost $2 billion in debt, or an average of $85,000 each. Their average take-home pay is around $3,300.

They are in this state not because they are clueless about money matters. More than 60 per cent of them have an A-level education or higher, and 12 per cent live in five-room Housing Board flats or private properties. Around 25 per cent own cars.

Half of them are in this state because they overspend. Financial advisers note that those who do this usually rely on credit cards to pay for a lifestyle that they cannot afford with their regular incomes.

But this does not mean they are splurging on expensive items. The overspending can be moderate and gradual, such as not setting a budget for regular shopping and dining or taking too many short breaks overseas that might cost only $1,000 or $2,000.

While they would normally be able to afford such expenses if they spent in moderation, they choose to let the debt roll over on credit cards by making only the minimum repayments.

As they continue to do so without keeping an eye on their income, the original debt and the increasing interest begin to grow until these people can no longer clear them on their own.

As CCS notes, this can happen to anyone, even those with high salaries, if their expenditure is disproportionate to their income.

CCS cases also reveal another unhealthy trend – that of people not managing their monthly finances prudently.

While almost 9,000 of them may not overspend, their outlays, including monthly mortgage payments and other expenses, are too close to their regular incomes.

This is a precarious situation because if they suffer pay cuts or worse, lose their jobs, they will immediately find themselves unable to keep up with their expenses.

Many of those who ask to defer loan repayments are probably in this state because their income has been affected by the downturn.

Housing-related loans play a substantial role in causing people to fall into the debt cycle. For instance, more than 4,000 people sought help from CCS because they had problems paying for home renovation and furnishing loans.

Gambling is commonly thought to be a cause of debt, but only about 15 per cent of CCS’ cases say they have dabbled in it.

An even smaller percentage, about 7 per cent, say they lost money on the stock market.

NEED TO WATCH WHAT YOU SPEND

As routine lifestyle expenses are the common reason people end up in high debt, CCS general manager Tan Huey Min urges families not to spend on expensive and non-essential items, especially during this downturn.

Cutting back does not mean your families have to face hardship.

It simply means spending according to what you can afford. You can still have fun doing so.

For instance, you can allocate a fixed sum each month for such expenses and the whole family can decide how they want to spend it.

This way, families will always spend within their means.

Ms Tan also advises families to think twice about using credit cards to fund their desired lifestyles.

“Never treat the credit facility as your supplementary income or savings. And don’t make the mistake of making impulsive purchases of expensive items with credit cards,” she says.

Many of the cases CCS handles involves the overuse of credit cards. This is why one of the strict requirements for those who seek its help is that they must terminate their cards.

So if you have the tendency to overspend and do not want to fall into a debt trap, you may want to start by always paying off the total amount charged to your credit card in full and to pay on time every month.